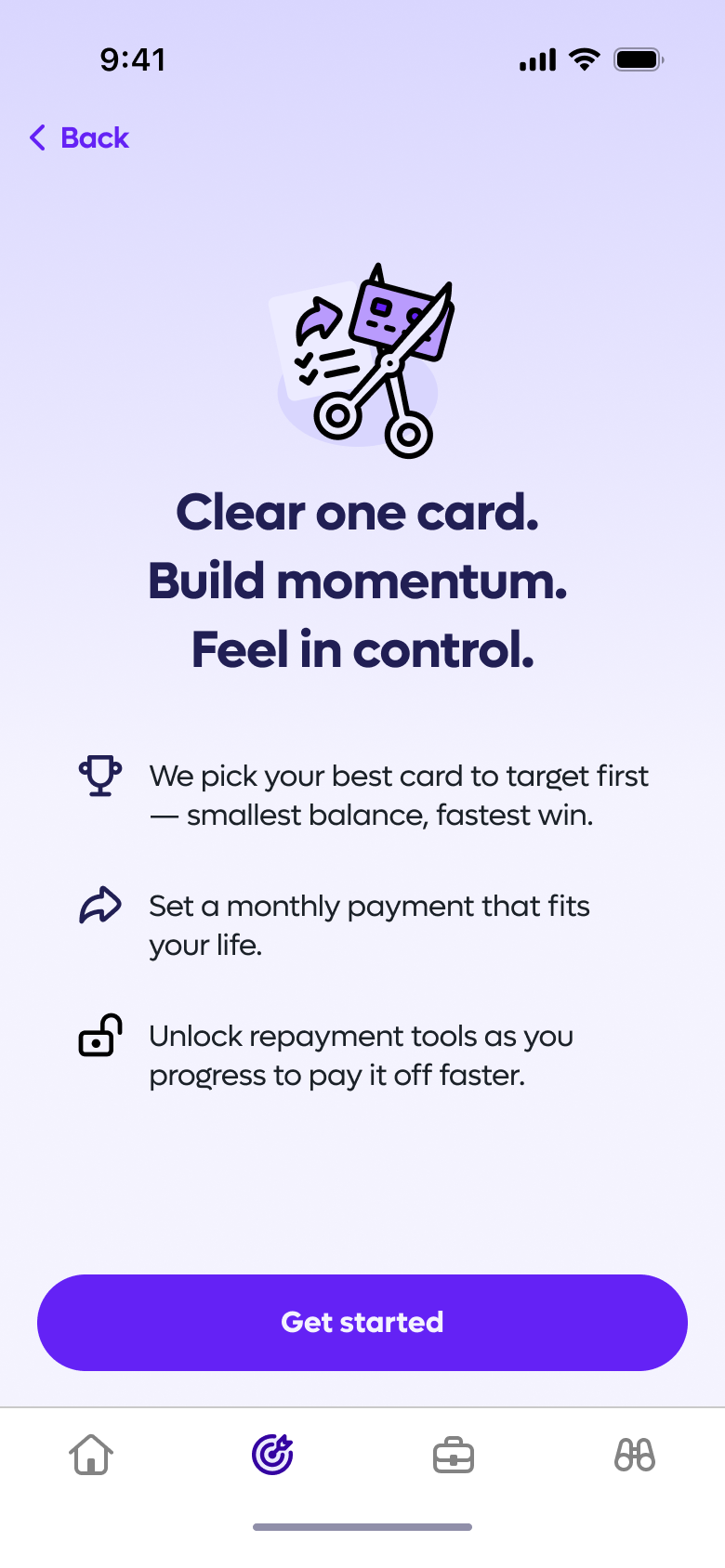

Clear One Card Repayment Plan

A guided repayment tool that reduces complexity and increases the number of CPay users actively paying down their credit card debt.

of users created a repayment plan with at least the recommended monthly payment — and said they'd do the same in a live app.

60%

KPI 1 - Recommended repayment plan adoption

of users set up spending round-ups to passively clear debt faster, understood how it worked — and said they'd use it in a live app.

60%

KPI 2 - Round-ups repayment activation

Thresholds: Success ≥ 70% | Accept 55–69% | Fail < 55%

Threshold: Pass ≥ 60% | Fail < 60%

Project Overview

Duration:

6 weeks

Type:

Freelance

Company:

CPay

Role:

Lead Product Designer

Deliverables:

Research and synthesis, design development and delivery

Collaborators:

Product Manager, Founder

Approach:

Double Diamond

Company Context

- CPay is a fintech startup rethinking how people manage credit card debt

- Their mission is to make borrowing fairer and less overwhelming through Open Banking and intelligent automation

- The product is an AI-powered app that connects your credit cards, analyses your spending and repayment patterns, and recommends smarter ways to get out of debt faster

Problem Statement

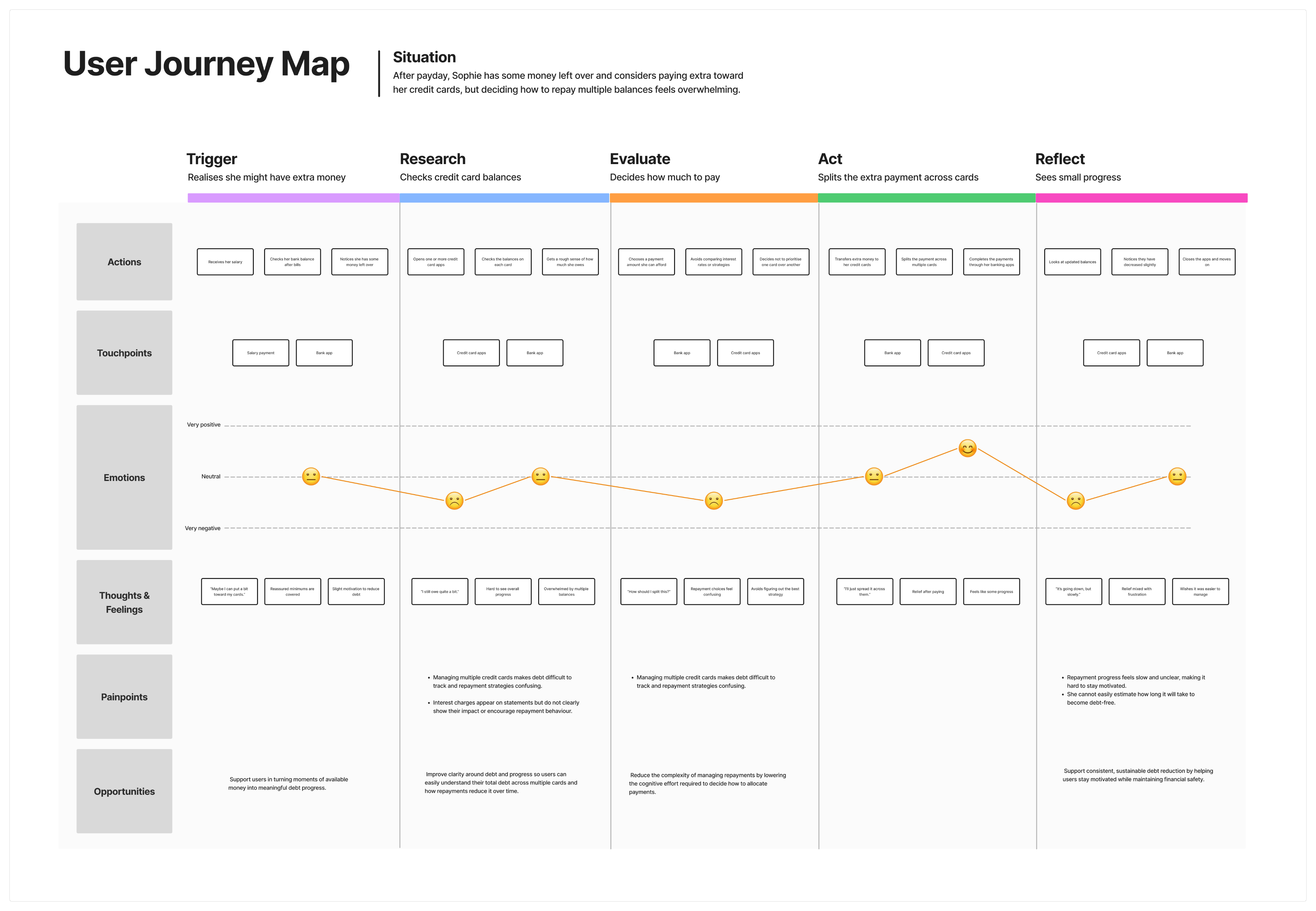

Someone managing multiple debts needs a way to confidently decide how to allocate repayments, so they can steadily reduce what they owe — without it becoming an overwhelming mental exercise.

Goals

Business

Reduce interest paid per user and improve repayment completion rates

Design

Make repayment plans easy to understand, build user confidence, and feel satisfying to set up

Success Metrics

Business

Reduce interest paid per user and improve repayment completion rates

Design

Make repayment plans easy to understand, build user confidence, and feel satisfying to set up

My Role

- Owned the design end-to-end, from early research to production-ready assets

- Worked closely with the PM to agree on success metrics upfront

- Ran workshops and regular stakeholder check-ins to keep everyone aligned

- Presented decisions to senior leadership and iterated based on their feedback

Process

- Interviewed stakeholders to understand the brief and align on goals

- Spoke with 12 users to uncover their real pain points

- Ran affinity mapping and built a persona to define the core problem

- Benchmarked 5+ competitors to spot gaps and opportunities

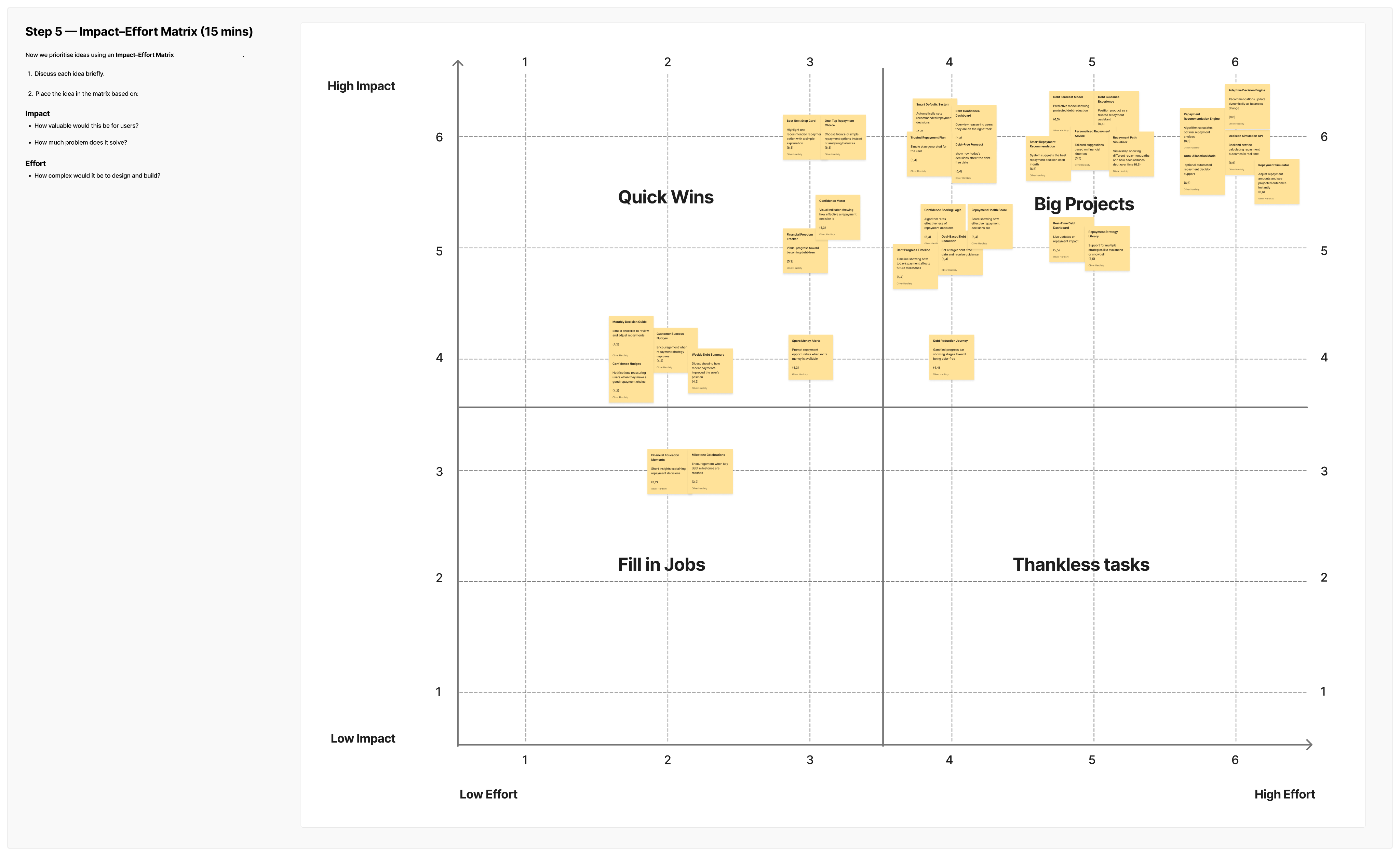

- Ran HMW workshops with the team to explore and prioritise ideas

- Tested designs with users across 2 rounds, iterating on findings

Problem Research

Key Research Insights

Insight 1

Simplicity beats strategy

Users default to easy repayment patterns to avoid cognitive load.

Evidence

Participants split payments evenly rather than comparing interest rates.

Insight 2

No clear debt end date

Payoff timelines feel too complex to calculate.

Evidence

Most participants had never estimated time to full repayment.

Insight 3

Progress drives motivation

Visible milestones keep users engaged and on track.

Evidence

Participants described motivation from watching balances shrink.

Insight 4

Interest feels abstract

Monthly charges feel too small to act on.

Evidence

Participants noticed interest but rarely adjusted behaviour in response.

Insight 5

Financial safety first

Savings buffers feel safer than accelerating repayment.

Evidence

Participants limited payments to protect a savings cushion.

key Research Deliverables

Persona

As-Is User Journey Map

Design Ideation

Lorem

[Caption]

[Caption]

[Caption]

[Caption]

Hypothesis

Subtitle

We believe that ....

By providing clear repayment guidance and showing the impact of repayment decisions, for the Simplicity Seeker, we will enable them to make confident repayment decisions with less cognitive effort.

We will know this to be true when we see ...

- Users following the recommended repayment option

- Users reporting that the repayment process feels easy to understand

- Users reporting higher confidence in their repayment choices

User Flows

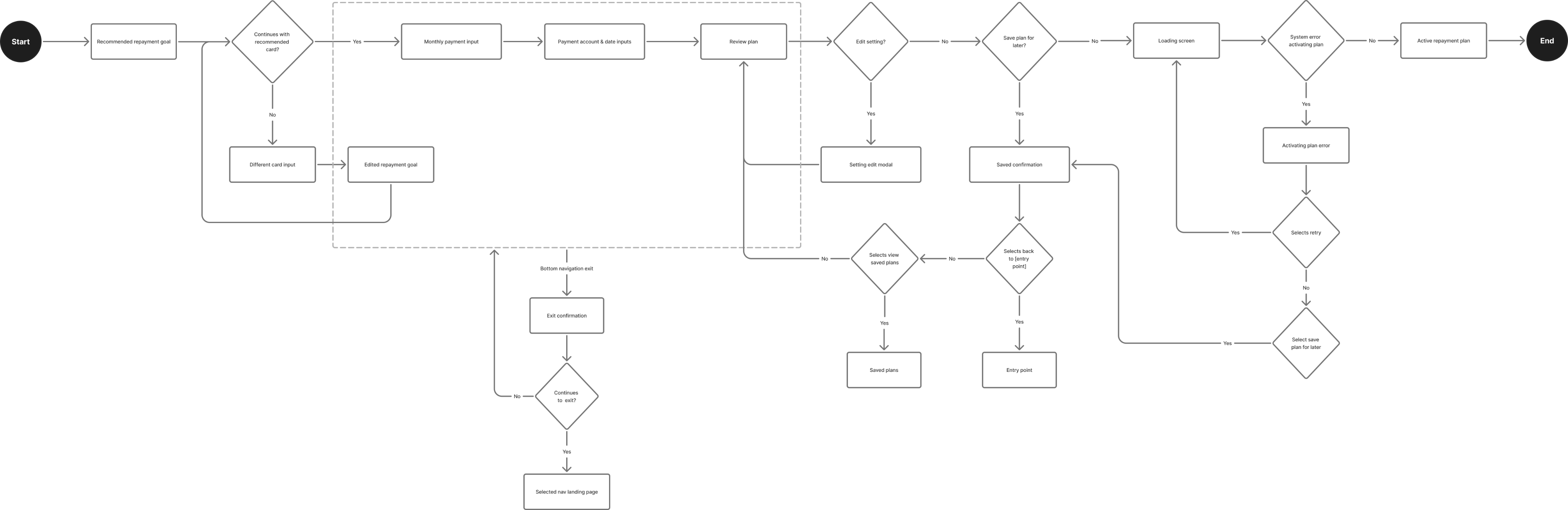

Create Repayment Plan - High-level flow

Create Repayment Plan - User flow

Prototyping &

Iterating

Prototype Usability Testing

Ran unmoderated remote usability testing using 5 screened participants. The test included:

- 2 prototype tasks: creating a repayment plan and activating round-up repayments.

- Post-task survey per prototype capturing ease of use, behavioural intent, and comprehension.

Subtitle

of users created a repayment plan with at least the recommended monthly payment — and said they'd do the same in a live app.

60%

KPI 1 - Recommended repayment plan adoption

of users set up spending round-ups to passively clear debt faster, understood how it worked — and said they'd use it in a live app.

60%

KPI 2 - Round-ups repayment activation

Thresholds: Success ≥ 70% | Accept 55–69% | Fail < 55%

Threshold: Pass ≥ 60% | Fail < 60%

Design Issues & Successes

design issue

Multi-card anxiety unresolved

One card targeted, others ignored — multi-card users feel partially addressed.

design issue

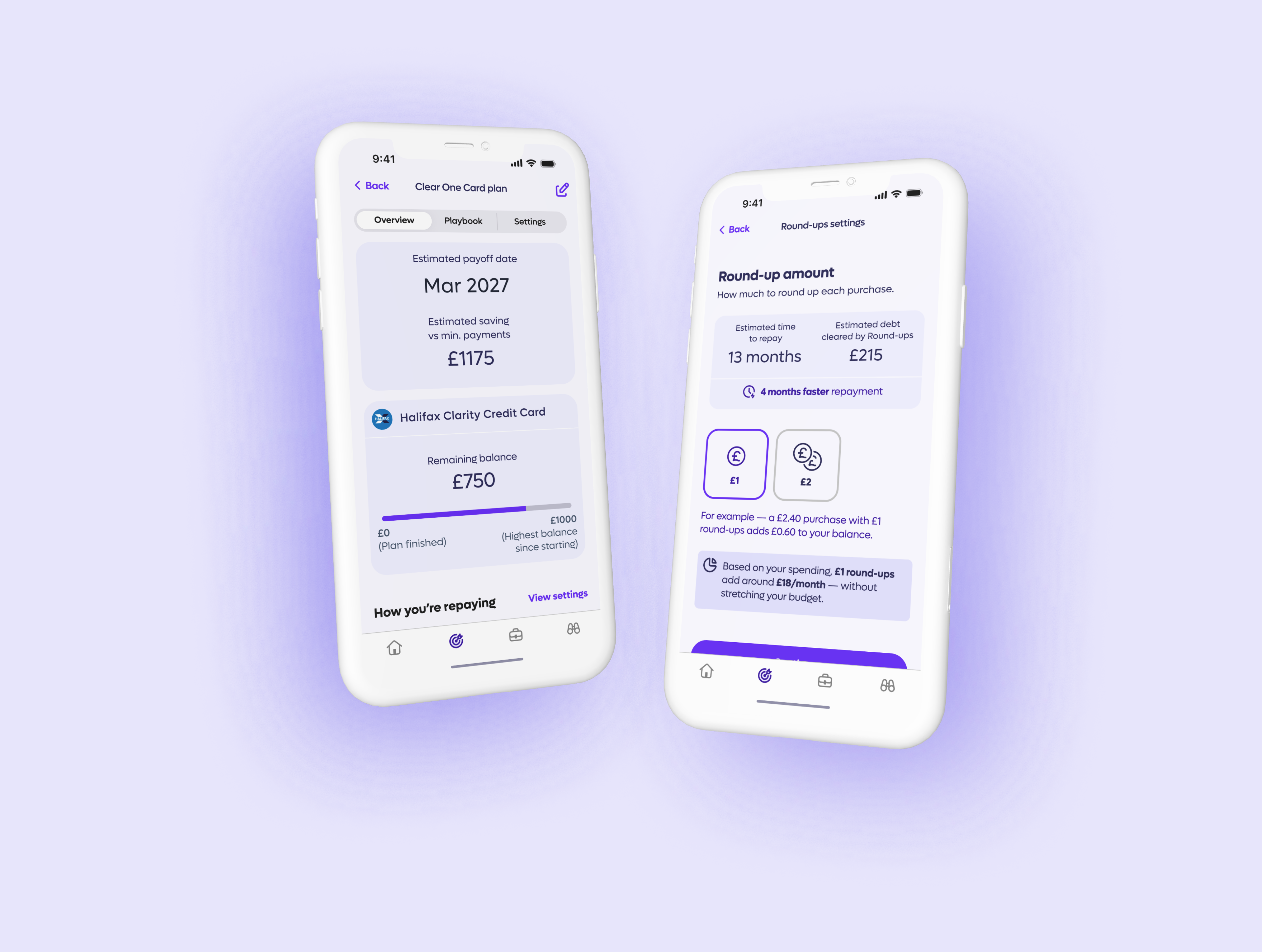

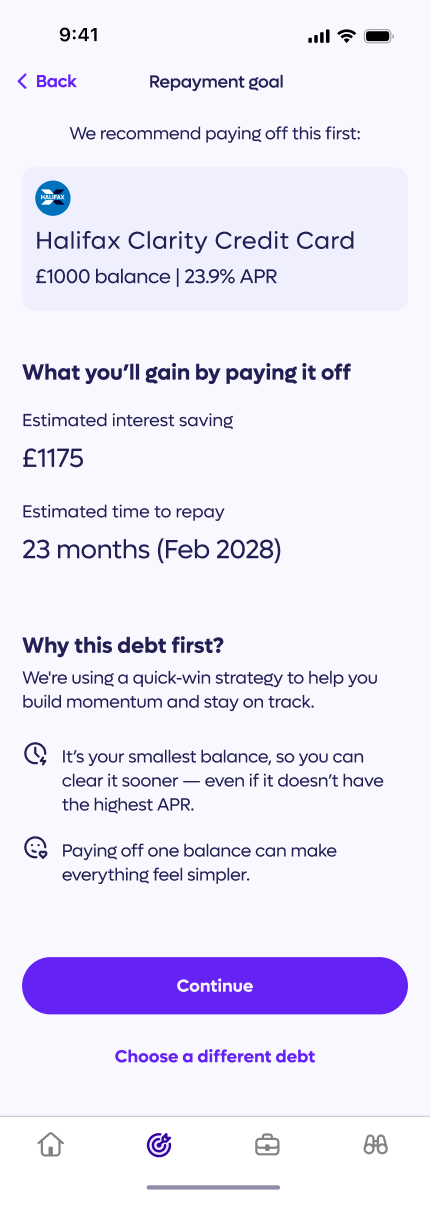

Repayment Goal payoff date appears absolute

"23 months (Feb 2028)" is presented as fixed before the user has set their payment amount.

design success

Finish-date framing lands consistently

Payoff dates outperform interest savings as the primary motivator across all users.

design success

Snowball rationale resolves "why this card"

"Why this debt first?" pre-empts the most common objection before users ask it.

design issue

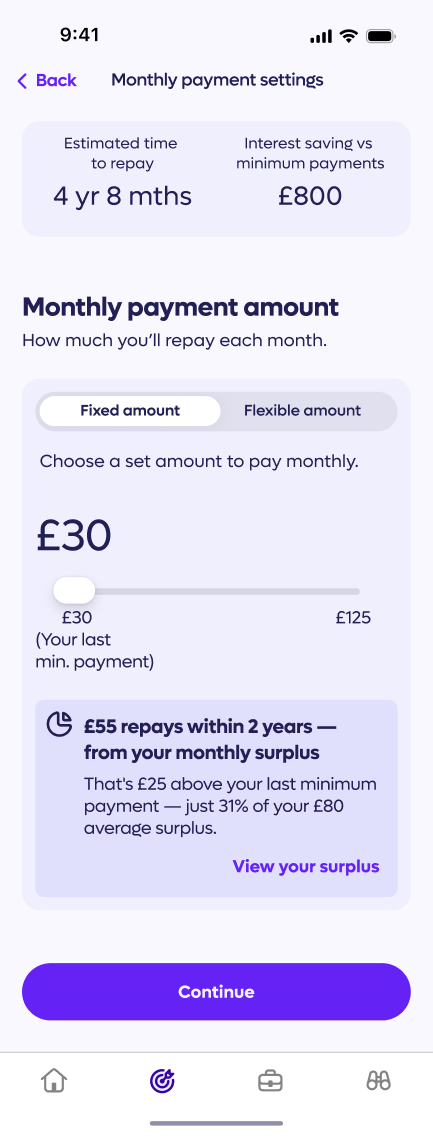

Slider default anchors payment too low

£30 default and surplus overlay's worst-month figure pull cautious users below the 24-month payoff threshold.

design success

Surplus framing reduces perceived cost

Framing £55 as 31% of existing surplus positions the increase as reallocation, not new expenditure.

design success

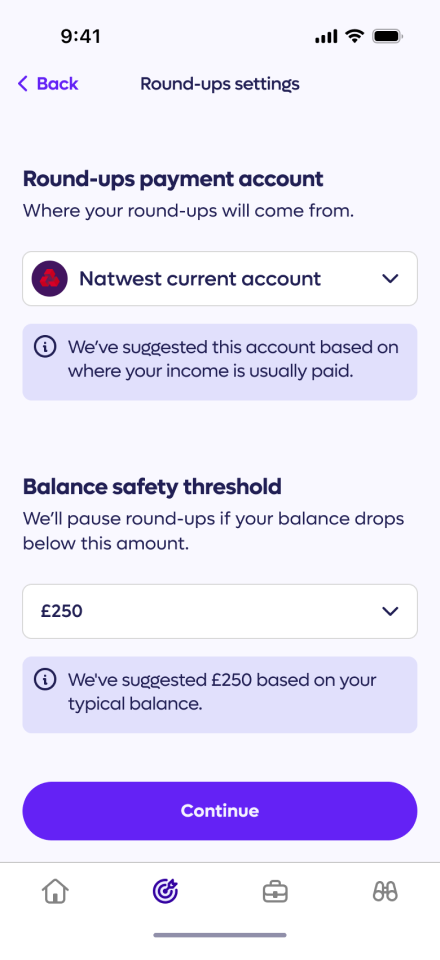

Pre-filled defaults remove friction

Intelligent account and date pre-selection makes the payment settings screen effectively invisible.

design success

Safety buffer framing outperforms restriction language

"Leaves a buffer" positions the cap as protective

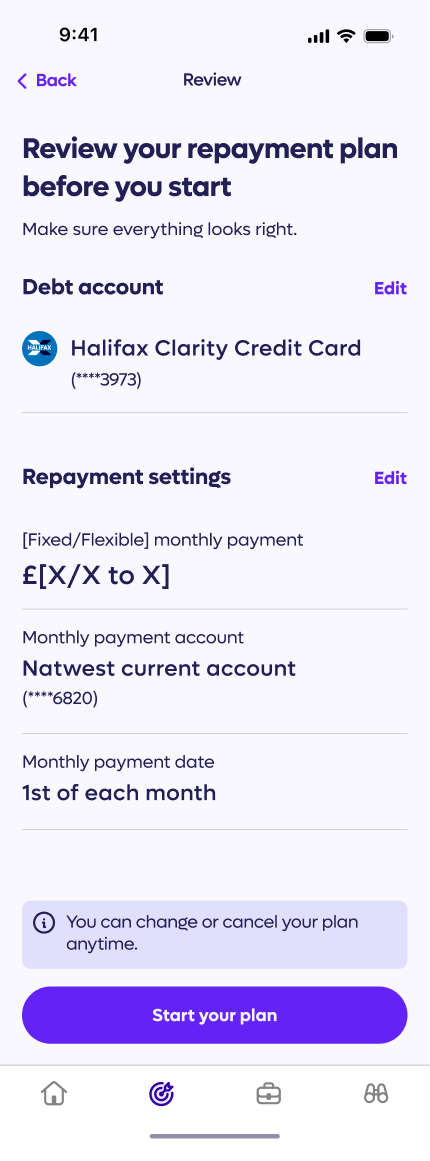

design issue

Review screen lacks payoff date

The strongest motivator is absent at the final commitment moment.

design success

No payment authority confirmation

Account and payment details collected with no explicit confirmation of what's been authorised.

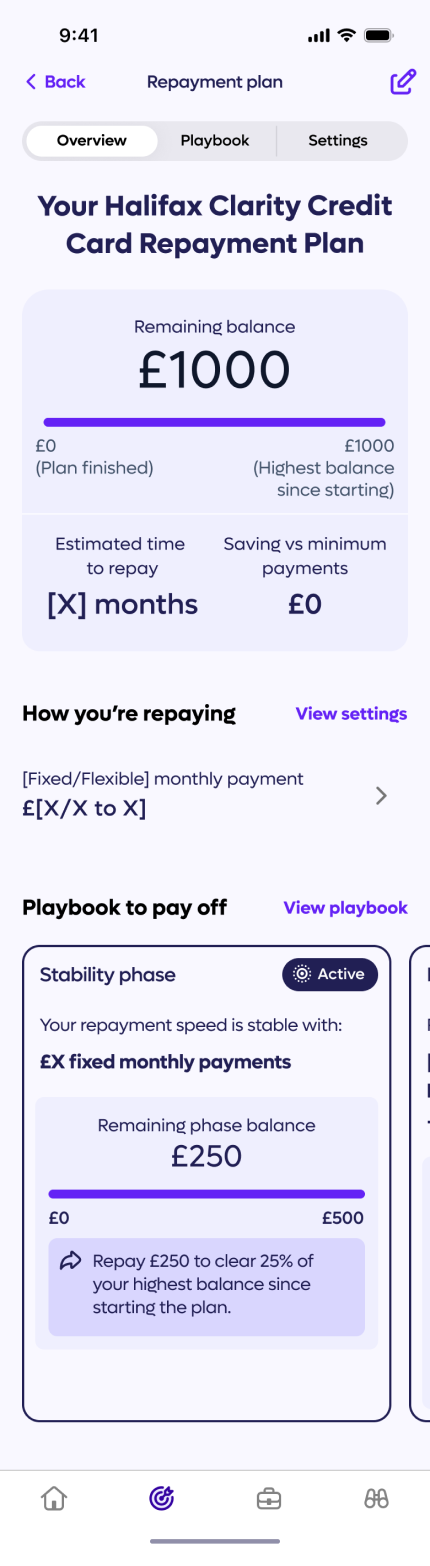

design issue

Dashboard placeholders undermine confirmation moment

Templated values at plan creation signal incompleteness at the most critical retention moment.

design success

Stability phase milestone is concrete and actionable

£250 near-term target chunks a multi-year repayment into a visible first goal.

design success

Playbook structure signals progression without overwhelming

Locked future phases generate curiosity, not anxiety.

Prototypes

Vibe coded with Figma Make to maximise realism and validity of insights.

Create Repayment Plan (KPI 1)

Prototype

Video

Activate Round-ups (KPI 2)

Prototype

Video

Outcomes & Lessons

Impact

All results were drawn from the final round of usability testing on fully coded prototypes — the most realistic signal of how the design performs in practice.

of users created a repayment plan with at least the recommended monthly payment — and said they'd do the same in a live app.

60%

Recommended repayment plan adoption

KPI 1

- Plan created with at least the recommended monthly payment amount

- Payoff date correctly identified

- Behavioural intent rated ≥ 4/5

Thresholds: Success ≥ 85% | Accept 70–84% | Fail < 70%

Conditions required to include users in the result:

of users set up spending round-ups to passively clear debt faster, understood how it worked — and said they'd use it in a live app.

60%

Round-ups repayment activation

KPI 2

- Round-ups set up for their plan

- How the feature works correctly explained

- Behavioural intent rated ≥ 4/5

Conditions required to include users in the result:

Threshold: Pass ≥ 60% | Fail < 60%

Key Learnings

Through this project, I particularly learnt the value of the following:

Aligning through stakeholder interviews

Interrogated briefs and aligned on client expectations before diving into design.

Grounding decisions in personas

Synthesised research to keep design choices focused and user-centred.

Defining success metrics

Set considered metrics upfront to drive iteration and measure outcomes.

Vibe coding for insight

Used vibe coding to surface meaningful patterns from user testing sessions.

If you like what you see

— Don’t be a stranger! ...

o.hardisty@me.com

Clear One Card Repayment Plan

A guided repayment tool that reduces complexity and increases the number of CPay users actively paying down their credit card debt.

of users created a repayment plan with at least the recommended monthly payment — and said they'd do the same in a live app.

60%

KPI 1 - Recommended repayment plan adoption

of users set up spending round-ups to passively clear debt faster, understood how it worked — and said they'd use it in a live app.

60%

KPI 2 - Round-ups repayment activation

Thresholds: Success ≥ 70% | Accept 55–69% | Fail < 55%

Threshold: Pass ≥ 60% | Fail < 60%

Project Overview

Duration:

6 weeks

Type:

Freelance

Company:

CPay

Role:

Lead Product Designer

Deliverables:

Research and synthesis, design development and delivery

Collaborators:

Product Manager, Founder

Approach:

Double Diamond

Company Context

- CPay is a fintech startup rethinking how people manage credit card debt

- Their mission is to make borrowing fairer and less overwhelming through Open Banking and intelligent automation

- The product is an AI-powered app that connects your credit cards, analyses your spending and repayment patterns, and recommends smarter ways to get out of debt faster

Problem Statement

Someone managing multiple debts needs a way to confidently decide how to allocate repayments, so they can steadily reduce what they owe — without it becoming an overwhelming mental exercise.

Goals

Business

Reduce interest paid per user and improve repayment completion rates

Design

Make repayment plans easy to understand, build user confidence, and feel satisfying to set up

Success Metrics

Business

Reduce interest paid per user and improve repayment completion rates

Design

Make repayment plans easy to understand, build user confidence, and feel satisfying to set up

My Role

- Owned the design end-to-end, from early research to production-ready assets

- Worked closely with the PM to agree on success metrics upfront

- Ran workshops and regular stakeholder check-ins to keep everyone aligned

- Presented decisions to senior leadership and iterated based on their feedback

Process

- Interviewed stakeholders to understand the brief and align on goals

- Spoke with 12 users to uncover their real pain points

- Ran affinity mapping and built a persona to define the core problem

- Benchmarked 5+ competitors to spot gaps and opportunities

- Ran HMW workshops with the team to explore and prioritise ideas

- Tested designs with users across 2 rounds, iterating on findings

Problem Research

Key Research Insights

Insight 1

Simplicity beats strategy

Users default to easy repayment patterns to avoid cognitive load.

Evidence

Participants split payments evenly rather than comparing interest rates.

Insight 2

No clear debt end date

Payoff timelines feel too complex to calculate.

Evidence

Most participants had never estimated time to full repayment.

Insight 3

Progress drives motivation

Visible milestones keep users engaged and on track.

Evidence

Participants described motivation from watching balances shrink.

Insight 4

Interest feels abstract

Monthly charges feel too small to act on.

Evidence

Participants noticed interest but rarely adjusted behaviour in response.

Insight 5

Financial safety first

Savings buffers feel safer than accelerating repayment.

Evidence

Participants limited payments to protect a savings cushion.

key Research Deliverables

Persona

As-Is User Journey Map

Design Ideation

Lorem

[Caption]

[Caption]

[Caption]

[Caption]

Hypothesis

Subtitle

We believe that ....

By providing clear repayment guidance and showing the impact of repayment decisions, for the Simplicity Seeker, we will enable them to make confident repayment decisions with less cognitive effort.

We will know this to be true when we see ...

- Users following the recommended repayment option

- Users reporting that the repayment process feels easy to understand

- Users reporting higher confidence in their repayment choices

User Flows

Create Repayment Plan - High-level flow

Create Repayment Plan - User flow

Prototyping &

Iterating

Prototype Usability Testing

Ran unmoderated remote usability testing using 5 screened participants. The test included:

- 2 prototype tasks: creating a repayment plan and activating round-up repayments.

- Post-task survey per prototype capturing ease of use, behavioural intent, and comprehension.

Subtitle

of users created a repayment plan with at least the recommended monthly payment — and said they'd do the same in a live app.

60%

KPI 1 - Recommended repayment plan adoption

of users set up spending round-ups to passively clear debt faster, understood how it worked — and said they'd use it in a live app.

60%

KPI 2 - Round-ups repayment activation

Thresholds: Success ≥ 70% | Accept 55–69% | Fail < 55%

Threshold: Pass ≥ 60% | Fail < 60%

Design Issues & Successes

design issue

Multi-card anxiety unresolved

One card targeted, others ignored — multi-card users feel partially addressed.

design issue

Repayment Goal payoff date appears absolute

"23 months (Feb 2028)" is presented as fixed before the user has set their payment amount.

design success

Finish-date framing lands consistently

Payoff dates outperform interest savings as the primary motivator across all users.

design success

Snowball rationale resolves "why this card"

"Why this debt first?" pre-empts the most common objection before users ask it.

design issue

Slider default anchors payment too low

£30 default and surplus overlay's worst-month figure pull cautious users below the 24-month payoff threshold.

design success

Surplus framing reduces perceived cost

Framing £55 as 31% of existing surplus positions the increase as reallocation, not new expenditure.

design success

Pre-filled defaults remove friction

Intelligent account and date pre-selection makes the payment settings screen effectively invisible.

design success

Safety buffer framing outperforms restriction language

"Leaves a buffer" positions the cap as protective

design issue

Review screen lacks payoff date

The strongest motivator is absent at the final commitment moment.

design success

No payment authority confirmation

Account and payment details collected with no explicit confirmation of what's been authorised.

design issue

Dashboard placeholders undermine confirmation moment

Templated values at plan creation signal incompleteness at the most critical retention moment.

design success

Stability phase milestone is concrete and actionable

£250 near-term target chunks a multi-year repayment into a visible first goal.

design success

Playbook structure signals progression without overwhelming

Locked future phases generate curiosity, not anxiety.

Prototypes

Vibe coded with Figma Make to maximise realism and validity of insights.

Create Repayment Plan (KPI 1)

Prototype

Video

Activate Round-ups (KPI 2)

Prototype

Video

Screen Flow Diagrams

Hover the screen flows to take a closer look

Create Repayment Plan

Happy path only

Click to zoom in and out

Activate Round-ups

Happy path only

Click to zoom in and out

Outcomes & Lessons

Impact

All results were drawn from the final round of usability testing on fully coded prototypes — the most realistic signal of how the design performs in practice.

of users created a repayment plan with at least the recommended monthly payment — and said they'd do the same in a live app.

60%

Recommended repayment plan adoption

KPI 1

- Plan created with at least the recommended monthly payment amount

- Payoff date correctly identified

- Behavioural intent rated ≥ 4/5

Thresholds: Success ≥ 85% | Accept 70–84% | Fail < 70%

Conditions required to include users in the result:

of users set up spending round-ups to passively clear debt faster, understood how it worked — and said they'd use it in a live app.

60%

Round-ups repayment activation

KPI 2

- Round-ups set up for their plan

- How the feature works correctly explained

- Behavioural intent rated ≥ 4/5

Conditions required to include users in the result:

Threshold: Pass ≥ 60% | Fail < 60%

Key Learnings

Through this project, I particularly learnt the value of the following:

Aligning through stakeholder interviews

Interrogated briefs and aligned on client expectations before diving into design.

Grounding decisions in personas

Synthesised research to keep design choices focused and user-centred.

Defining success metrics

Set considered metrics upfront to drive iteration and measure outcomes.

Vibe coding for insight

Used vibe coding to surface meaningful patterns from user testing sessions.

If you like what you see — Don’t be a stranger! ...

o.hardisty@me.com

Clear One Card Repayment Plan

A guided repayment tool that reduces complexity and increases the number of CPay users actively paying down their credit card debt.

of users created a repayment plan with at least the recommended monthly payment — and said they'd do the same in a live app.

60%

KPI 1 - Recommended repayment plan adoption

of users set up spending round-ups to passively clear debt faster, understood how it worked — and said they'd use it in a live app.

60%

KPI 2 - Round-ups repayment activation

Thresholds: Success ≥ 70% | Accept 55–69% | Fail < 55%

Threshold: Pass ≥ 60% | Fail < 60%

Project Overview

Duration:

6 weeks

Type:

Freelance

Company:

CPay

Role:

Lead Product Designer

Deliverables:

Research and synthesis, design development and delivery

Collaborators:

Product Manager, Founder

Approach:

Double Diamond

Company Context

- CPay is a fintech startup rethinking how people manage credit card debt

- Their mission is to make borrowing fairer and less overwhelming through Open Banking and intelligent automation

- The product is an AI-powered app that connects your credit cards, analyses your spending and repayment patterns, and recommends smarter ways to get out of debt faster

Problem Statement

Someone managing multiple debts needs a way to confidently decide how to allocate repayments, so they can steadily reduce what they owe — without it becoming an overwhelming mental exercise.

Goals

Business

Reduce interest paid per user and improve repayment completion rates

Design

Make repayment plans easy to understand, build user confidence, and feel satisfying to set up

Success Metrics

Two KPIs were defined — one per prototype. Each KPI has three conditions, that had to be met simultaneously to count as a conversion.

KPI 1 — Recommended repayment plan adoptionPercentage of users who created a repayment plan that met the following conditions:

- Plan created with at least the recommended monthly payment amount

- Payoff date correctly identified

- Behavioural intent rated ≥ 4/5

Thresholds: Success ≥ 70% | Accept 55–69% | Fail < 55%

KPI 2 — Round-ups repayment activationPercentage of users who activated round-ups. A pass required:

- Round-ups set up for their plan

- How the feature works correctly explained

- Behavioural intent rated ≥ 4/5

Threshold: Pass ≥ 60% | Fail < 60%

My Role

- Owned the design end-to-end, from early research to production-ready assets

- Worked closely with the PM to agree on success metrics upfront

- Ran workshops and regular stakeholder check-ins to keep everyone aligned

- Presented decisions to senior leadership and iterated based on their feedback

Process

- Interviewed stakeholders to understand the brief and align on goals

- Spoke with 12 users to uncover their real pain points

- Ran affinity mapping and built a persona to define the core problem

- Benchmarked 5+ competitors to spot gaps and opportunities

- Ran HMW workshops with the team to explore and prioritise ideas

- Tested designs with users across 2 rounds, iterating on findings

Problem Research

Key Research Insights

Insight 1

Simplicity beats strategy

Users default to easy repayment patterns to avoid cognitive load.

Evidence

Participants split payments evenly rather than comparing interest rates.

Insight 2

No clear debt end date

Payoff timelines feel too complex to calculate.

Evidence

Most participants had never estimated time to full repayment.

Insight 3

Progress drives motivation

Visible milestones keep users engaged and on track.

Evidence

Participants described motivation from watching balances shrink.

Insight 4

Interest feels abstract

Monthly charges feel too small to act on.

Evidence

Participants noticed interest but rarely adjusted behaviour in response.

Insight 5

Financial safety first

Savings buffers feel safer than accelerating repayment.

Evidence

Participants limited payments to protect a savings cushion.

key Research Deliverables

Persona

As-Is User Journey Map

Design Ideation

Lorem

Ideation

Hypothesis

Subtitle

We believe that ....

By providing clear repayment guidance and showing the impact of repayment decisions, for the Simplicity Seeker, we will enable them to make confident repayment decisions with less cognitive effort.

We will know this to be true when we see ...

- Users following the recommended repayment option

- Users reporting that the repayment process feels easy to understand

- Users reporting higher confidence in their repayment choices

User Flows

Create Repayment Plan - High-level flow

Create Repayment Plan - User flow

Prototyping &

Iterating

Prototype Usability Testing

Ran unmoderated remote usability testing using 5 screened participants. The test included:

- 2 prototype tasks: creating a repayment plan and activating round-up repayments.

- Post-task survey per prototype capturing ease of use, behavioural intent, and comprehension.

Subtitle

of users created a repayment plan with at least the recommended monthly payment — and said they'd do the same in a live app.

60%

KPI 1 - Recommended repayment plan adoption

of users set up spending round-ups to passively clear debt faster, understood how it worked — and said they'd use it in a live app.

60%

KPI 2 - Round-ups repayment activation

Thresholds: Success ≥ 70% | Accept 55–69% | Fail < 55%

Threshold: Pass ≥ 60% | Fail < 60%

Design Issues & Successes

design issue

Multi-card anxiety unresolved

One card targeted, others ignored — multi-card users feel partially addressed.

design issue

Repayment Goal payoff date appears absolute

"23 months (Feb 2028)" is presented as fixed before the user has set their payment amount.

design success

Finish-date framing lands consistently

Payoff dates outperform interest savings as the primary motivator across all users.

design success

Snowball rationale resolves "why this card"

"Why this debt first?" pre-empts the most common objection before users ask it.

design issue

Slider default anchors payment too low

£30 default and surplus overlay's worst-month figure pull cautious users below the 24-month payoff threshold.

design success

Surplus framing reduces perceived cost

Framing £55 as 31% of existing surplus positions the increase as reallocation, not new expenditure.

design success

Pre-filled defaults remove friction

Intelligent account and date pre-selection makes the payment settings screen effectively invisible.

design success

Safety buffer framing outperforms restriction language

"Leaves a buffer" positions the cap as protective

design issue

Review screen lacks payoff date

The strongest motivator is absent at the final commitment moment.

design success

No payment authority confirmation

Account and payment details collected with no explicit confirmation of what's been authorised.

design issue

Dashboard placeholders undermine confirmation moment

Templated values at plan creation signal incompleteness at the most critical retention moment.

design success

Stability phase milestone is concrete and actionable

£250 near-term target chunks a multi-year repayment into a visible first goal.

design success

Playbook structure signals progression without overwhelming

Locked future phases generate curiosity, not anxiety.

Prototypes

Vibe coded with Figma Make to maximise realism and validity of insights.

Create Repayment Plan (KPI 1)

Prototype

Video

Activate Round-ups (KPI 2)

Prototype

Video

Screen Flow Diagrams

Hover the screen flows to take a closer look

Create Repayment Plan

Happy path only

Click to zoom in and out

Activate Round-ups

Happy path only

Click to zoom in and out

Outcomes & Lessons

Impact

All results were drawn from the final round of usability testing on fully coded prototypes — the most realistic signal of how the design performs in practice.

of users created a repayment plan with at least the recommended monthly payment — and said they'd do the same in a live app.

60%

Recommended repayment plan adoption

KPI 1

- Plan created with at least the recommended monthly payment amount

- Payoff date correctly identified

- Behavioural intent rated ≥ 4/5

Thresholds: Success ≥ 85% | Accept 70–84% | Fail < 70%

Conditions required to include users in the result:

of users set up spending round-ups to passively clear debt faster, understood how it worked — and said they'd use it in a live app.

60%

Round-ups repayment activation

KPI 2

- Round-ups set up for their plan

- How the feature works correctly explained

- Behavioural intent rated ≥ 4/5

Conditions required to include users in the result:

Threshold: Pass ≥ 60% | Fail < 60%

Key Learnings

Through this project, I particularly learnt the value of the following:

Aligning through stakeholder interviews

Interrogated briefs and aligned on client expectations before diving into design.

Grounding decisions in personas

Synthesised research to keep design choices focused and user-centred.

Defining success metrics

Set considered metrics upfront to drive iteration and measure outcomes.

Vibe coding for insight

Used vibe coding to surface meaningful patterns from user testing sessions.

If you like what you see — Don’t be a stranger! ...

o.hardisty@me.com